Why we invest in the Dumb, Dull, Dirty & Dangerous at CT Capital

We spend our time at Contrarian Thinking Capital in the unglamorous, fragmented parts of the economy:

List of industries that will produce the most valuable SaaS companies of the next decade:

• HVAC

• Roofing

• Painting

• Recycling

• Plumbing

• Electrical

• Warehousing

• Laundromats

• Car washes

• Construction

• Pest control

• Landscaping

• Property services

• Cleaning services

• Handyman services

• Waste management

• 3PL / cross-docking

• Maritime operations

• Facilities maintenance

• Freight (trucking, SMB fleets)

• Garment care (dry cleaning)

• Middle market back-office and ops software

• Ports, drayage, and container logistics

• Field services (dispatch, scheduling, quoting, fleet, compliance)

The dumb, dull, dirty, and dangerous.

Dumb = overlooked everyday businesses with huge TAMs

Dull = work nobody wants to romanticize (low competition)

Dirty = exposure to undesired elements necessary to sustain livelihood

Dangerous = high-risk, labor-intensive environments

These are the systems everything else in our economy runs on. Most haven't been meaningfully touched by software in decades.

6 reasons we invest across this continuum:

1. The real economy is massively under-softwared

For the last 15 years, tech optimized the last mile.

Amazon perfected delivery

DoorDash handled food

Stripe simplified payments

All of it sits at the consumer-facing edge.

The first 80% (the part that builds, moves, installs, maintains, and powers things) changed little.

Construction sites still run on paper. Field service operators stitch together five tools that were never designed to talk to each other. These industries pay a fragmentation tax: too many disconnected systems, too much manual coordination, and no unified operating model.

Take Cents - building an all-in-one operating system for laundromats.

When they started, the industry ran on handwritten tickets. Human machine teaming was limited to the washing of clothes. To be fair, a large piece of the actual labor required touch, judgment, and care that only a human could provide. Yet still, Alex and team saw an opportunity that could handle the science of it. They rebuilt the entire operating model from scratch (POS, payments, machine monitoring, pickup routing, AI reception) into one system.

Now they power 1 in 12 laundromats in America.

2. Re-industrialization is creating a demand spike the existing workforce can't absorb

Manufacturing is coming back…fast.

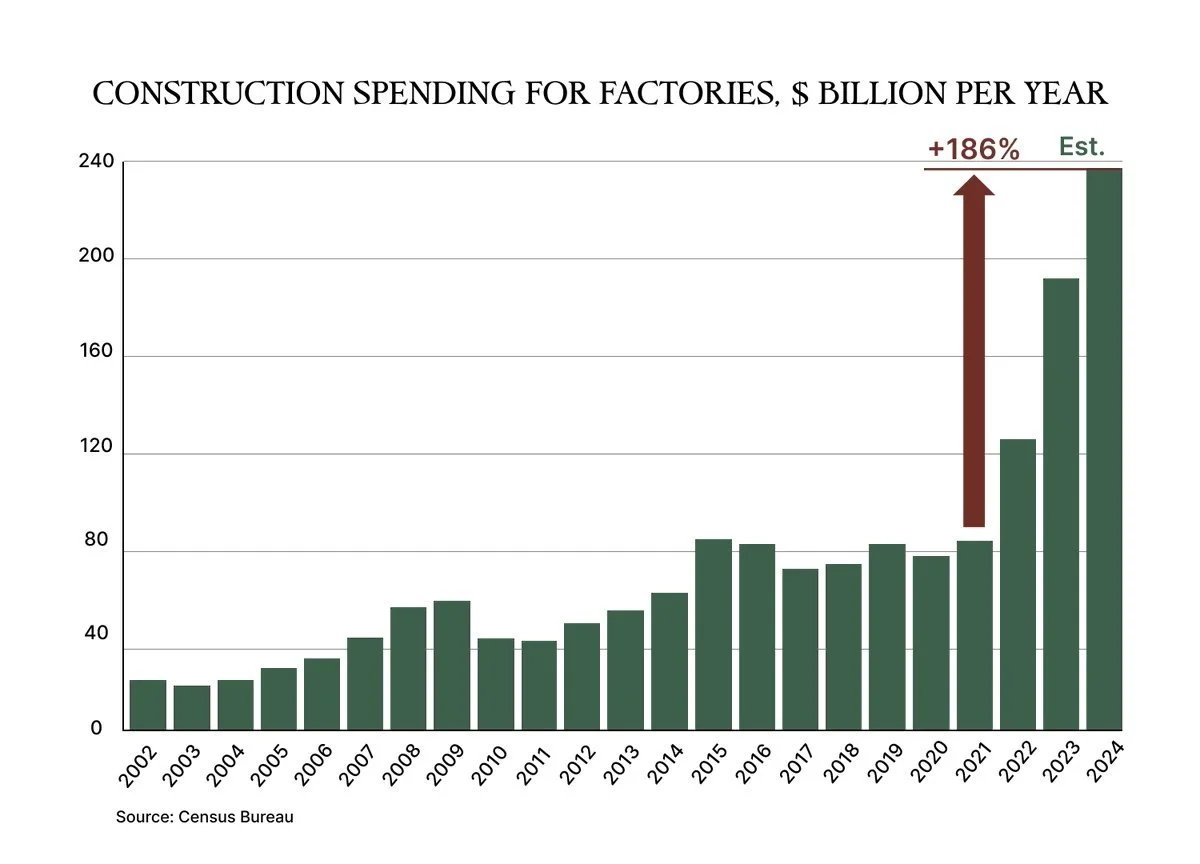

Factory construction spending hit $234B in 2024, up 186% from 2021.

244,000 manufacturing jobs were announced in 2024 alone through reshoring. The first million jobs took 10 years (2010-2020). The second million took 4 (2020-2024).

Industrial capacity is scaling but the physical systems beneath it are lagging behind.

The U.S. construction industry will need ~349,000 net new workers in 2026 and 456,000 in 2027 just to keep pace.

Meanwhile, 41% of the current workforce will retire by 2031.

Companies like Figure and Pave Robotics are at the helm of this dynamic.

Figure is building humanoid robots for factories and warehouses, deployed at BMW, now at a $39B valuation. They're filling critical labor gaps where workers either don’t exist or whose intellect is underutilized.

Pave automates road crack sealing. Crews work in traffic, exposed to the elements, harsh chemicals, and 2 ton metal-bodied missiles piloted by newly minted drivers, the distracted, and the oblivious. Pave's robot handles detection, cleaning, and sealing autonomously. Nobody will be required to risk their life on an active roadway.

3. The TAM is bigger than the "small business" label suggests

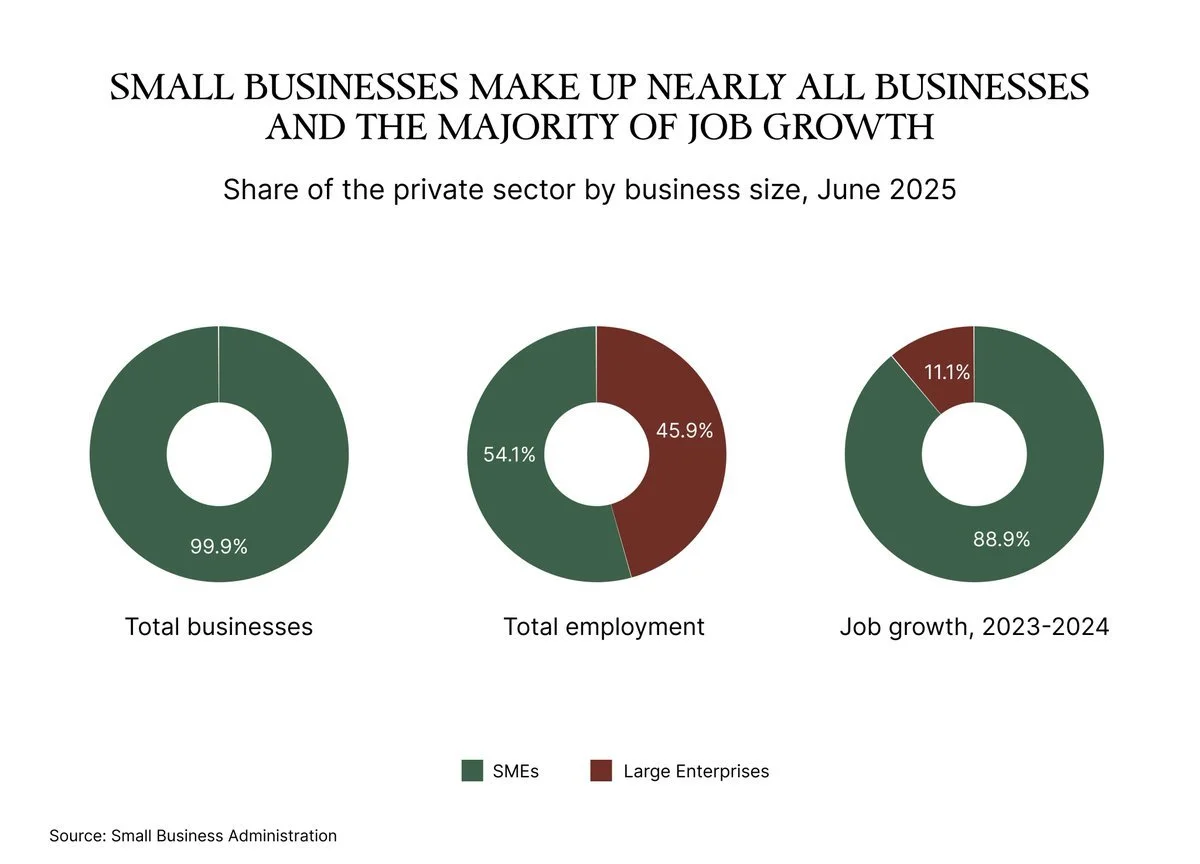

Silicon Valley calls laundromats, HVAC companies, and freight forwarders "small businesses" and moves on. That framing shrinks perceived TAM before the math.

36.2 million companies. 62 million Americans employed. 45.9% of the workforce.

Legacy industries constitute the majority: construction, transportation, waste management, field services, manufacturing, etc.

These industries are largely opposite the consumer market, demand here doesn't fluctuate; these are necessities where positioning and branding matters less than timeliness, efficiency, quality, and cost. We always need roads, power, water, buildings, and repairs. We rarely go label-shopping to choose.

This is a logical bet on enormous capital absorption, demand that doesn’t disappear, and no clear dominant software player.

4. Tech is giving small teams enterprise-level leverage

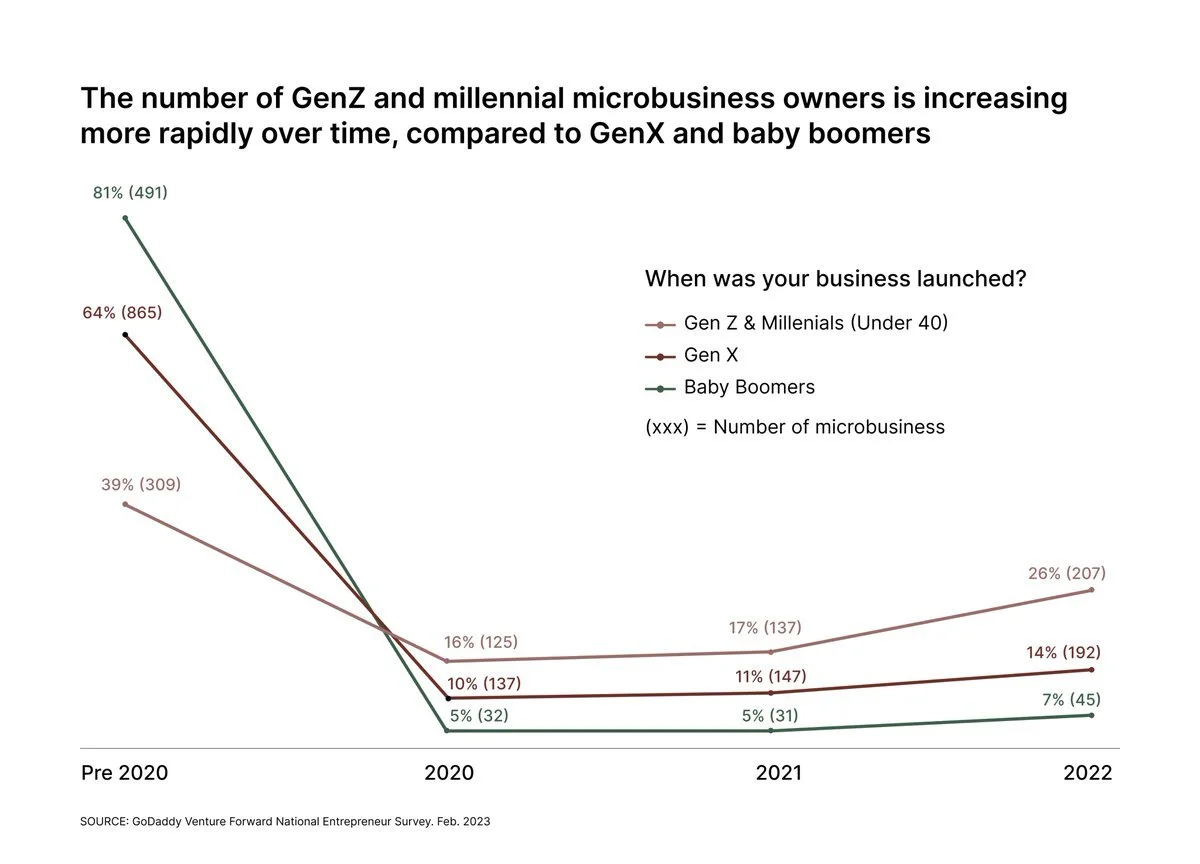

A laundromat operator in Iowa can now reach customers the same way a SaaS company in San Francisco does. That's new. The people taking over these businesses are digital-native in a way the previous generation wasn't.

An $84 trillion wealth transfer is underway as Boomers retire, $14T of which are business assets. In 2018, millennials owned roughly 7% to 10% of the SMB market. Today, they own approximately 13% and it is estimated that in 2030, they will own nearly 47%, and these operators expect software to run every part of the business: ops, marketing, finance, customer support.

A 5-7 person team, properly tooled, can now operate with the sophistication that once required 15+ people. This reduction in human capital will continue to increase as data collection mechanisms are refined, tools integrate and industries modernize.

The software to make that possible is only just arriving.

5. Customers here only pay for things that work

42% of small-cap public companies in the Russell 2000 are unprofitable.

Small businesses don't have the luxury of operating at a loss. They have mere months to turn a profit, or they shut down. No venture subsidy. No runway to “figure it out”. Structural pivots won’t work for a welder.

That creates a completely different buyer.

Operators in the 4Ds only pay for tools that reduce costs, increase throughput, or solve a lingering constraint. Impact must be measured and immediate. System’s ability to naturally orchestrate up and down the chain is no longer a convenience, it’s an expectation. Inherent network effects to upstream and downstream partners will be a

Drillbit built an AI employee, Mason, for trades and franchise operators that runs leads, scheduling, follow-ups, and customer ops end-to-end.

They're driving 148% conversion lifts and 2.89x profit margin increases.

That's what survival looks like in this market. And that discipline, forced on the software company by the customer, is what produces durable, infrastructure-like businesses.

The profit constraint of the buyer creates the moat for the seller.

6. These problems don’t go away

Ten years from now, AI-powered vanity apps will go the way of the high churn, ad-farming, attention grabbing games…but roads will always crack, inventory will be managed, pipes will break, and machines will fail.

The companies solving for the first mile now will become the infrastructure layer of the economy.

If you're building in the dumb, dull, dirty, or dangerous, DMs are open. Contact me today.